Maximize Your Retirement Benefits: 2026 401(k) & IRA Limits

Anúncios

The latest projections for 2026 retirement contribution limits indicate that Americans may see modest increases in tax-advantaged savings thresholds for both 401(k) and IRA accounts. Expected adjustments from the Internal Revenue Service are tied to inflation trends and cost-of-living calculations, helping savers preserve long-term retirement purchasing power.

In the field of retirement planning, these annual contribution limit updates are considered essential for maximizing tax efficiency and long-term investment growth. Higher contribution caps can provide additional opportunities for workers to strengthen retirement savings, especially for individuals utilizing employer-sponsored plans and catch-up contributions.

Looking ahead, financial analysts recommend monitoring official IRS announcements and reviewing contribution strategies early in the year. Understanding projected 401(k) and IRA limits can help individuals optimize savings plans, improve portfolio growth potential, and better prepare for long-term retirement goals in 2026.

Anúncios

Understanding the 2026 401(k) Contribution Limits

The 401(k) remains a cornerstone of employer-sponsored retirement plans, offering significant tax advantages for employees.

For 2026, projections indicate an increase in the maximum contribution limits, reflecting ongoing inflation adjustments and economic growth. These changes are vital for employees planning their annual savings strategies.

Anúncios

Employers and employees must pay close attention to these new limits, as exceeding them can lead to tax penalties and administrative complications.

The updated figures provide a fresh opportunity for individuals to reassess their current contribution rates and adjust them upwards to retirement benefits.

These adjustments are typically announced by the IRS in the latter part of the preceding year, giving individuals and plan administrators ample time to prepare. Understanding the nuances of these limits, including catch-up contributions for older workers, is key to effective financial planning.

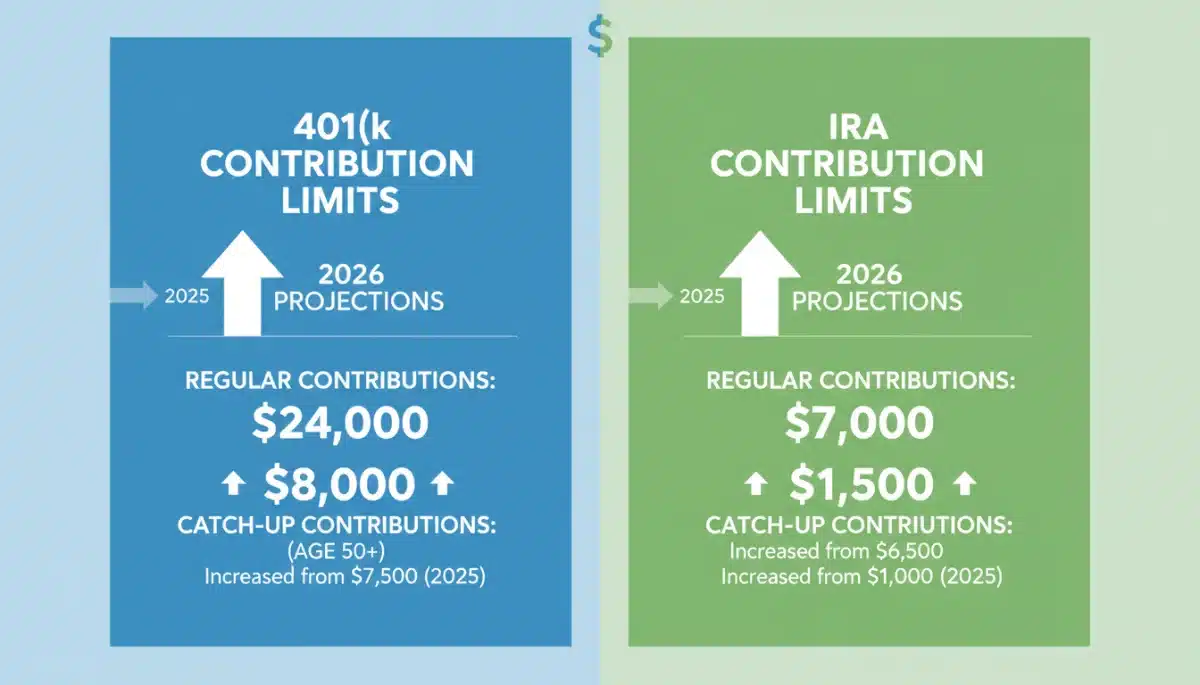

Projected Standard 401(k) Contributions for 2026

Based on current economic trends and historical adjustment patterns, the standard 401(k) contribution limit for employees is expected to see a notable increase.

This rise is designed to help maintain the purchasing power of retirement savings against inflation. It gives individuals more capacity to save for their future.

For many, this projected increase represents a direct opportunity to accelerate their retirement savings goals. Maximizing this standard contribution is often the first step in a comprehensive retirement strategy. It’s a fundamental way to leverage tax-deferred growth.

- Expected increase of approximately $500 to $1,000 from current limits.

- This adjustment reflects the IRS’s annual cost-of-living indexing.

- Employers should communicate these changes clearly to their workforce.

2026 401(k) Catch-Up Contributions for Older Workers

The catch-up contribution provision allows individuals aged 50 and over to contribute an additional amount to their 401(k)s, recognizing their shorter time horizon until retirement. For 2026, this catch-up limit is also anticipated to increase, providing a significant boost for those nearing retirement.

This additional contribution is a powerful tool for individuals who may have started saving later in their careers or wish to accelerate their savings in their peak earning years. It significantly enhances the ability to retirement benefits.

Financial advisors often recommend that eligible individuals take full advantage of these catch-up provisions. It’s a strategic move to bolster retirement funds and capitalize on tax advantages during crucial pre-retirement years. These contributions can make a substantial difference in overall retirement security.

Anticipated 2026 IRA Contribution Limits

Individual Retirement Arrangements (IRAs) offer another critical avenue for retirement savings, providing flexibility and various tax benefits. Similar to 401(k)s, IRA contribution limits are also subject to annual adjustments by the IRS, with 2026 expected to bring new thresholds.

These changes apply to both Traditional and Roth IRAs, impacting a broad spectrum of savers. Understanding the new IRA limits is essential for individuals to plan their contributions effectively, especially for those who do not have access to an employer-sponsored plan or wish to supplement their 401(k) savings.

The projected increases underscore the importance of regular review of personal financial plans. Adapting to these new limits ensures that individuals are continuously optimizing their tax-advantaged savings and working towards their retirement objectives.

Projected Standard IRA Contributions for 2026

The standard IRA contribution limit for 2026 is projected to see an upward revision, offering individuals more room to save on a tax-advantaged basis. This increase is a direct response to economic indicators and the IRS’s commitment to adjust limits for inflation. It benefits millions of American savers.

Whether you contribute to a Traditional IRA, which offers tax-deductible contributions, or a Roth IRA, where qualified withdrawals are tax-free in retirement, these new limits are crucial. Maximizing these contributions is a fundamental strategy to retirement benefits.

- Expected increase of approximately $500 from current limits.

- Applies to both Traditional and Roth IRA contributions.

- Consider income limitations for Roth IRA contributions and Traditional IRA deductibility.

2026 IRA Catch-Up Contributions for Those 50 and Over

For individuals aged 50 and above, the IRA catch-up contribution provision allows for additional savings beyond the standard limit. This provision is expected to remain a powerful tool for enhanced retirement savings in 2026, with potential for a slight adjustment.

This flexibility is particularly valuable for those who are accelerating their retirement planning in later career stages. Taking full advantage of these catch-up contributions can significantly boost one’s retirement nest egg. It’s an often-underutilized benefit that can yield substantial long-term gains.

While the catch-up contribution amount for IRAs has historically been static for several years, any adjustment for 2026 would further amplify its impact. Eligible individuals should factor this into their savings strategy to truly retirement benefits.

Strategic Planning to Maximize Your Benefits

Beyond simply knowing the limits, strategic planning is essential to fully leverage the 2026 contribution allowances for 401(k)s and IRAs. This involves a comprehensive review of your financial situation, understanding your employer’s matching contributions, and considering various account types.

Effective planning ensures that you are not just contributing, but contributing smartly to retirement benefits. This includes evaluating your tax situation to determine whether a Traditional or Roth account is more beneficial for your specific circumstances.

Consulting with a financial advisor can provide personalized guidance, helping you navigate the complexities of retirement planning and optimize your contributions. Their expertise can ensure your strategy aligns with your long-term financial goals and risk tolerance.

Leveraging Employer 401(k) Matches

One of the most straightforward ways to boost your retirement savings is to contribute enough to your 401(k) to receive the full employer match. This is essentially free money and is a critical component of any sound retirement strategy. Many employees overlook this significant benefit.

Failing to take advantage of an employer match leaves substantial money on the table, directly hindering your ability to retirement benefits. It’s a guaranteed return on your investment that is hard to beat.

- Identify your employer’s specific matching formula.

- Adjust your contribution rate to meet the maximum match threshold.

- Consider increasing contributions beyond the match if financially feasible.

The Roth vs. Traditional Decision for 2026

Deciding between a Roth and Traditional IRA or 401(k) depends heavily on your current income, projected future income, and tax outlook. Each option offers distinct tax advantages that can be optimized based on individual circumstances. This choice significantly impacts your long-term tax liability.

A Traditional IRA or 401(k) offers tax-deductible contributions now, while a Roth provides tax-free withdrawals in retirement. The optimal choice helps to retirement benefits, aligning with your personal financial trajectory.

For those expecting to be in a higher tax bracket in retirement, a Roth account might be more advantageous. Conversely, if you expect to be in a lower tax bracket in retirement, a Traditional account could offer better current tax savings. This decision requires careful consideration.

Impact of Economic Factors on 2026 Limits

The adjustment of retirement contribution limits is not arbitrary; it’s a direct consequence of various economic factors, primarily inflation and wage growth. These elements play a pivotal role in how the IRS calculates and implements the annual changes, ensuring the limits remain relevant.

Understanding the underlying economic drivers helps contextualize the anticipated 2026 changes. It also provides insight into future adjustments, enabling more proactive and informed financial planning. This economic perspective is crucial for long-term strategizing.

The Bureau of Labor Statistics’ Consumer Price Index (CPI) and other economic indicators are closely monitored by the IRS. These metrics directly influence the cost-of-living adjustments that lead to higher contribution limits, allowing individuals to retirement benefits.

Inflation and Cost-of-Living Adjustments

Inflation is a primary driver behind the annual increases in retirement contribution limits. As the cost of living rises, the IRS adjusts these limits to ensure that the real value of retirement savings is maintained. This protects retirees’ purchasing power.

The adjustments are designed to prevent inflation from eroding the effectiveness of retirement accounts. Higher limits mean individuals can save more tax-advantaged dollars, which is essential in a dynamic economic environment. It’s a mechanism to keep pace with economic realities.

- Limits are indexed to inflation, typically using the CPI.

- Higher inflation often leads to larger increases in contribution limits.

- These adjustments are vital for maintaining the real value of retirement savings.

Wage Growth and its Influence

Wage growth also plays a significant role in the determination of retirement contribution limits. As average wages increase, so does the capacity for individuals to save more for retirement. The IRS considers these trends to set appropriate limits.

Strong wage growth often correlates with a healthy economy, which in turn supports higher contribution limits. This allows individuals to effectively retirement benefits, reflecting their increased earning potential.

Monitoring national wage growth reports can provide early indications of potential adjustments to retirement limits. This forward-looking approach can help individuals anticipate changes and refine their savings strategies accordingly for the upcoming year.

Advanced Strategies for Retirement Savings

Beyond simply maximizing annual contributions, several advanced strategies can further enhance your retirement savings. These include utilizing Backdoor Roth IRAs, Mega Backdoor Roth conversions, and strategic asset allocation. These tactics require a deeper understanding of tax codes and financial planning principles.

These advanced methods are particularly beneficial for high-income earners who might face restrictions on direct Roth IRA contributions. They offer pathways to inject more capital into tax-advantaged accounts, helping to truly retirement benefits.

Implementing these strategies often requires careful consideration and, ideally, guidance from a qualified financial professional. The complexities involved necessitate expert advice to ensure compliance and optimal outcomes for your specific situation.

Backdoor Roth and Mega Backdoor Roth Strategies

The Backdoor Roth IRA strategy allows high-income earners who exceed the Roth IRA income limits to still contribute to a Roth account. This involves contributing to a Traditional IRA (non-deductible) and then converting it to a Roth IRA, paying taxes on any gains.

The Mega Backdoor Roth is an even more advanced strategy, typically available through 401(k) plans that allow after-tax contributions. These after-tax contributions can then be converted to a Roth 401(k) or rolled into a Roth IRA, significantly increasing tax-free retirement savings. These methods are powerful tools to retirement benefits.

Understanding the rules and potential pitfalls of these strategies is crucial. They can be complex and are subject to IRS regulations, making professional advice invaluable for proper execution and avoiding unintended tax consequences. It’s important to ensure these strategies align with your overall financial objectives.

Diversification and Asset Allocation

Effective asset allocation and diversification are fundamental to long-term retirement savings success. Spreading investments across various asset classes—such as stocks, bonds, and real estate—helps mitigate risk and optimize returns over time. This strategy is critical regardless of contribution limits.

As you approach 2026 and beyond, regularly reviewing and rebalancing your portfolio according to your risk tolerance and time horizon is essential. A well-diversified portfolio complements your efforts to retirement benefits by ensuring your savings grow efficiently.

Consider your investment goals and consult with a financial professional to create an asset allocation strategy that aligns with your individual circumstances. This proactive approach to portfolio management can significantly impact the ultimate value of your retirement nest egg. It’s about smart growth, not just saving.

The Role of Financial Advisors in 2026 Planning

Navigating the complexities of retirement planning, especially with evolving contribution limits and tax codes, can be challenging. Financial advisors play a crucial role in providing tailored guidance, helping individuals make informed decisions that align with their specific financial goals.

A good financial advisor can offer personalized strategies, clarify tax implications, and help you implement advanced savings techniques. Their expertise is invaluable for those looking to effectively retirement benefits.

They can also help you stay updated on regulatory changes and market fluctuations, ensuring your retirement plan remains robust and adaptable. Engaging with a professional financial advisor is an investment that can yield significant returns in the form of enhanced financial security and peace of mind.

Personalized Retirement Strategies

Every individual’s financial situation, risk tolerance, and retirement goals are unique. A financial advisor can develop a personalized retirement strategy that takes into account your specific circumstances. This bespoke approach goes beyond generic advice.

They can help you determine the optimal contribution levels for your 401(k) and IRA, evaluate the best investment vehicles, and plan for potential future expenses. Such tailored guidance is essential to truly retirement benefits.

- Assess your current financial health and future projections.

- Recommend appropriate investment strategies and account types.

- Help set realistic and achievable retirement savings goals.

Staying Informed on Tax Law Changes

Tax laws related to retirement accounts can be complex and are subject to change. Financial advisors stay abreast of these legislative developments, ensuring that your retirement planning remains compliant and optimized for tax efficiency. This vigilance protects your savings from unforeseen tax liabilities.

They can explain how proposed or enacted tax law changes might impact your contributions, withdrawals, and overall retirement income. This proactive approach helps you adapt your strategy in time to retirement benefits.

Regular consultations with your advisor can keep you informed about any new opportunities or restrictions. This ongoing dialogue ensures that your retirement plan is always aligned with the latest tax regulations and economic conditions, providing stability and potential growth.

| Key Point | Brief Description |

|---|---|

| 2026 401(k) Limits | Projected increases for standard and catch-up contributions due to inflation. |

| 2026 IRA Limits | Anticipated rise in standard IRA limits for both Traditional and Roth accounts. |

| Strategic Planning | Utilize employer matches, choose Roth vs. Traditional, and consider advanced strategies. |

| Expert Guidance | Financial advisors offer personalized strategies and tax law insights. |

Frequently Asked Questions About 2026 Retirement Limits

The IRS typically announces the official contribution limits for the upcoming year in late October or early November of the preceding year. This allows individuals and financial institutions sufficient time to prepare and adjust their plans accordingly. These announcements are eagerly awaited by financial planners.

No, the projected limits are based on current economic forecasts and historical trends but are not guaranteed. The actual limits will be officially announced by the IRS. While projections are generally accurate, minor variations can occur based on final economic data and calculations.

Exceeding contribution limits can lead to tax penalties. For IRAs, excess contributions may be subject to a 6% excise tax each year they remain in the account. For 401(k)s, excess contributions are taxable in both the contribution year and the distribution year. It’s crucial to correct these errors promptly.

Yes, you can contribute to both a 401(k) and an IRA simultaneously. Each account has its own separate contribution limits. This dual approach can significantly boost your overall retirement savings, allowing you to leverage different tax advantages offered by each type of account.

The choice between Roth and Traditional depends on your current and projected future tax brackets. If you anticipate being in a higher tax bracket in retirement, Roth (tax-free withdrawals) is often preferred. If you expect a lower tax bracket in retirement, Traditional (current tax deduction) might be better. Consult a financial advisor for personalized advice.

Looking Ahead: Optimizing Your 2026 Retirement Strategy

The anticipated 2026 retirement contribution limits present a clear opportunity for individuals to refine and enhance their long-term financial strategies. Proactive engagement with these updated figures is not just beneficial but essential for securing a robust retirement. This forward-looking approach ensures you are prepared for future economic landscapes.

Monitoring official IRS announcements and consulting with financial professionals will be key steps in the coming months. These actions will help individuals fully understand and implement the most effective strategies to retirement benefits. Staying informed is the first line of defense against financial uncertainty.

Ultimately, a well-informed and adaptable retirement plan, leveraging the updated 2026 contribution limits, will empower you to build a secure financial future. The ability to retirement benefits hinges on continuous awareness and strategic adjustments to your savings approach.

in 2026")