Understanding Flexible Spending Accounts (FSAs) in 2026

This 2026 guide offers crucial insights into Flexible Spending Accounts (FSAs), detailing how individuals can strategically utilize these benefits for significant financial savings. It covers the latest changes, contribution limits, and eligible expenses to help optimize your healthcare and dependent care spending effectively.

Anúncios

Latest developments on Flexible Spending Accounts show higher 2026 limits, giving US workers more room to set aside pre-tax money for eligible healthcare and dependent care costs. The IRS raised the health FSA limit to $3,400, while the allowed carryover for plans that offer it increased to $680.

Dependent Care FSAs also received a major update for 2026, with the household limit rising to $7,500, creating a larger tax-saving opportunity for families paying for childcare or adult dependent care. These accounts remain valuable, but employees must plan carefully because many FSA balances are still subject to “use-it-or-lose-it” rules.

Readers should monitor employer enrollment deadlines, eligible expense lists, carryover rules, and IRS guidance before choosing their 2026 contribution amount. Experts recommend estimating predictable medical, dental, vision, and dependent care costs in advance to maximize savings without leaving unused funds behind.

Anúncios

Understanding the Fundamentals of Flexible Spending Accounts in 2026

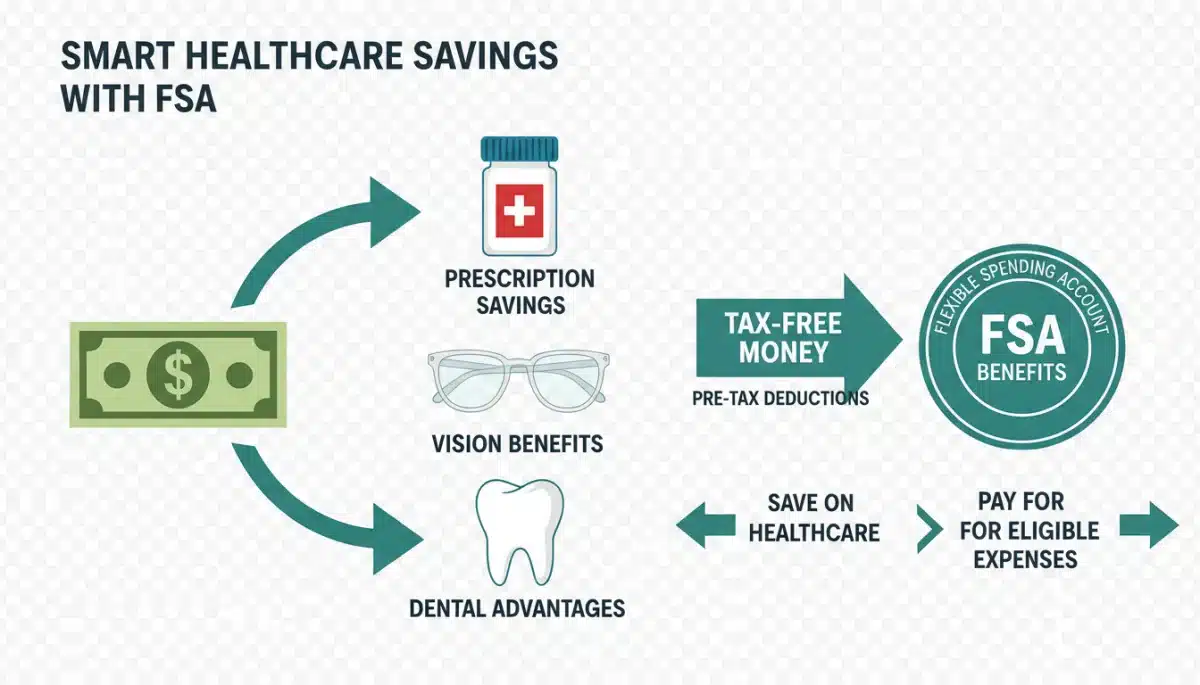

Flexible Spending Accounts (FSAs) allow employees to set aside pre-tax money from their paychecks to cover qualified medical or dependent care expenses. This pre-tax contribution effectively reduces taxable income, leading to significant savings for participants.

For 2026, it is crucial to review the updated contribution limits and any adjustments to eligible expenses, as these figures can impact your annual election. Employers typically provide open enrollment information detailing these specifics, which should be carefully considered.

The primary benefit of an Flexible Spending Accounts lies in its tax advantage, as funds are deducted before federal, state, and Social Security taxes are applied. This makes FSAs a powerful financial planning tool for anticipated healthcare and dependent care costs.

Anúncios

What is a Flexible Spending Account?

A Flexible Spending Account is an employer-sponsored benefit that enables you to allocate pre-tax dollars for specific expenses. These accounts are distinct from Health Savings Accounts (HSAs) and are generally associated with traditional health plans.

The funds contributed to an FSA are typically available at the beginning of the plan year, even if you haven’t fully contributed the amount yet. This front-loading of benefits can be a considerable advantage for immediate medical or dependent care needs.

It is important to note that FSAs are tied to your employment; if you leave your job, you generally lose access to the remaining funds, with some exceptions for COBRA or grace periods.

Key Differences: FSA vs. HSA

While both FSAs and HSAs offer tax advantages for health expenses, they have fundamental differences. FSAs are ‘use-it-or-lose-it’ (though some have carryover or grace period options), while HSAs are personal accounts that roll over year to year and are portable.

HSAs require enrollment in a High Deductible Health Plan (HDHP), whereas FSAs can be offered with almost any health insurance plan. Understanding these distinctions is vital for choosing the right account for your financial and health needs.

Another key difference is that HSA funds can be invested, potentially growing over time, while FSA funds are typically not invested. This makes HSAs a long-term savings vehicle, whereas Flexible Spending Accounts are designed for immediate, anticipated expenses.

2026 Contribution Limits and Eligibility

The IRS typically announces the new contribution limits for Flexible Spending Accounts late in the preceding year, usually in October or November. These limits dictate the maximum amount an individual can contribute to their FSA for the upcoming plan year.

Staying updated on these figures is essential for maximizing your pre-tax savings and ensuring compliance with federal regulations. Exceeding the limits can lead to tax implications and complications.

Eligibility for an FSA is generally tied to your employer’s benefits package; if your employer offers one, you can typically enroll during their open enrollment period. Self-employed individuals are not eligible for FSAs.

Anticipated Medical FSA Contribution Limits for 2026

While official 2026 figures are pending, historical trends suggest a modest increase from the previous year’s limits. For 2025, the medical FSA contribution limit was $3,200 per employee, per employer, indicating what might be expected for 2026.

This limit applies to each employee, meaning if both spouses work and their employers offer FSAs, they can each contribute up to the maximum amount. This can significantly increase a household’s total pre-tax savings for healthcare.

It is crucial to verify the exact 2026 limits once they are officially released by the IRS to ensure accurate planning and contributions. Consult your HR department or plan administrator for the most current information.

Dependent Care FSA Limits in 2026

Dependent Care FSAs (DCFSAs) have a separate set of contribution limits, which often remain more stable year-over-year compared to medical FSAs. For 2025, the limit was $5,000 per household ($2,500 if married filing separately).

These funds are specifically for eligible dependent care expenses, such as daycare, after-school programs, or elder care, allowing you to pay for these services with pre-tax dollars. This offers substantial savings for families with childcare costs.

The DCFSA limit is a per-household limit, not per employee, which is an important distinction when both spouses are employed. Careful planning is needed to avoid over-contributing to this account.

Eligible Expenses: What You Can Pay For

Understanding what expenses are eligible for reimbursement is key to maximizing your FSA. The IRS defines a broad range of qualified medical expenses, which often includes more than just doctor’s visits and prescriptions.

For Dependent Care FSAs, eligible expenses are specifically those incurred for the care of a qualifying child under age 13 or a spouse/dependent incapable of self-care. These expenses must allow you (and your spouse, if applicable) to work, look for work, or attend school full-time.

Reviewing the comprehensive list of eligible expenses provided by your plan administrator or the IRS is essential to avoid using funds on non-reimbursable items, which can incur penalties.

Qualified Medical Expenses for FSAs

Qualified medical expenses include a wide array of services and products, from deductibles, co-payments, and prescription medications to dental and vision care. Over-the-counter medications and certain medical supplies are also typically eligible.

Some less obvious eligible expenses can include acupuncture, chiropractic care, certain smoking cessation programs, and even breast pumps and supplies. Always check with your plan or the IRS for the most current list.

It is important to keep meticulous records and receipts for all expenses you plan to claim. This documentation is crucial for reimbursement and in case of an audit.

Eligible Dependent Care Expenses

Dependent Care FSA funds can be used for expenses directly related to the care of your qualifying dependents. This includes services like daycare centers, preschool, after-school programs, and even summer day camps.

Care provided by a nanny or au pair can also be eligible, provided they are not your spouse, your child under 19, or the parent of your qualifying child. The primary purpose of the care must be to enable you to work.

Expenses for overnight camps, schooling for kindergarten and above, or services primarily for education are generally not eligible. Always confirm with your plan administrator for specific covered services.

Navigating the ‘Use-It-or-Lose-It’ Rule and Its Exceptions

The traditional ‘use-it-or-lose-it’ rule is one of the most significant challenges for FSA participants. This rule mandates that any funds not spent by the end of the plan year are forfeited back to the employer.

However, many employers now offer exceptions to this rule, which can provide more flexibility. These exceptions include a grace period or a carryover option, both designed to mitigate the risk of losing funds.

Understanding whether your employer offers these exceptions, and how they work, is crucial for effective FSA planning and avoiding unnecessary forfeiture of your hard-earned money.

Grace Period Option

A grace period allows participants an extended period, typically up to two and a half months after the plan year ends, to incur and claim eligible FSA expenses. This provides a valuable buffer to spend down remaining balances.

For example, if your plan year ends on December 31st, a grace period might extend until March 15th of the following year. This extra time can be particularly useful for unexpected medical bills or last-minute purchases.

It is important to note that an employer can offer either a grace period or a carryover, but not both. Check your plan details carefully to determine which, if any, option is available to you.

FSA Carryover Option

The carryover option permits participants to roll over a limited amount of unused FSA funds into the next plan year. For 2025, the maximum carryover amount was $640, and a similar figure is expected for 2026.

This option provides more certainty than a grace period, as the funds are not lost but simply transferred to the new year. It helps reduce the pressure to spend every last dollar by the end of the year.

If your employer offers a carryover, you can still contribute the full maximum amount to your FSA for the new plan year, in addition to the carried-over funds. This makes the carryover a highly attractive feature for many.

Strategic Planning for Your 2026 FSA

Effective utilization of your 2026 FSA requires careful forecasting of your anticipated healthcare and dependent care needs. Over-contributing can lead to forfeiture, while under-contributing means missing out on tax savings.

Reviewing past medical expenses, considering any upcoming planned procedures, and assessing changes in dependent care needs are all critical steps. This proactive approach ensures your election aligns with your actual spending.

Many online tools and calculators can assist in estimating your annual expenses. Leveraging these resources can provide a more accurate picture of how much to contribute to your FSA.

Estimating Healthcare Expenses

To accurately estimate healthcare expenses, consider your deductible, co-pays, and anticipated prescription costs. Factor in any planned dental work, vision exams, or specialist visits for the upcoming year.

Think about recurring expenses, such as allergy medications or physical therapy, and any new health conditions that might arise. Don’t forget over-the-counter items like pain relievers, bandages, and first-aid supplies.

Looking at your prior year’s medical spending can offer a good baseline, but always adjust for any known changes in your health or insurance coverage for 2026.

Estimating Dependent Care Expenses

For Dependent Care FSAs, calculate your regular daycare or after-school care costs on an annual basis. Include any summer camp fees or other periodic dependent care expenses you anticipate.

If you have multiple dependents, remember the household limit applies, not a per-child limit. Ensure that the expenses are for care that enables you to work or look for work.

Consider any potential changes in your work schedule or your dependent’s needs that might impact care costs throughout 2026. Planning ahead minimizes the risk of unused funds.

Maximizing Your FSA: Tips and Best Practices

Beyond simply contributing, there are several best practices to ensure you get the most out of your Flexible Spending Account. These strategies focus on proactive management and timely utilization of funds.

Keeping organized records, understanding your plan’s specific rules, and initiating spending early in the plan year are all vital for successful FSA management. Don’t wait until the last minute to use your funds.

Regularly review your account balance and eligible expenses throughout the year to avoid a year-end scramble. This proactive approach helps prevent the dreaded ‘use-it-or-lose-it’ scenario.

Keeping Track of Expenses and Receipts

Maintaining meticulous records of all eligible expenses and corresponding receipts is paramount. Many FSA administrators offer mobile apps or online portals to upload and track your submissions easily.

These records are essential for submitting claims for reimbursement and for auditing purposes. Without proper documentation, your claims may be denied, or you could face tax penalties.

Establish a system, whether digital or physical, to store your receipts immediately after incurring an expense. This habit will save you significant time and stress later on.

Understanding Your Plan’s Specifics

Each employer’s FSA plan can have slightly different rules regarding claim submission deadlines, grace periods, or carryover amounts. It is crucial to read your plan’s Summary Plan Description (SPD) thoroughly.

Pay close attention to any specific requirements for documentation or types of eligible providers. Your HR department or FSA administrator is the best resource for clarifying any ambiguities.

Knowing your plan’s specific nuances will help you navigate the process smoothly and avoid any surprises when seeking reimbursement or managing your year-end balance.

Common Pitfalls to Avoid with Your 2026 FSA

While FSAs offer substantial benefits, certain pitfalls can diminish their value if not carefully managed. These often revolve around the ‘use-it-or-lose-it’ rule and misinterpreting eligible expenses.

One common mistake is over-contributing due to an overly optimistic estimate of annual expenses, leading to forfeited funds. Another is failing to submit claims on time, even for eligible expenses.

Being aware of these potential issues allows for proactive measures to mitigate risks and ensure you fully benefit from your Flexible Spending Accounts contributions.

Over-Contributing to Your Flexible Spending Accounts

Contributing too much to your Flexible Spending Accounts is a significant pitfall, especially if your plan does not offer a generous carryover or grace period. Once funds are elected, they are generally locked in for the plan year.

If your actual expenses fall short of your elected amount, you risk losing the unspent portion. This underscores the importance of careful and realistic expense estimation at the time of enrollment.

Consider a slightly conservative estimate if you are unsure of your exact expenses, particularly if your employer does not offer a carryover or grace period option. You can always pay for additional expenses out-of-pocket if needed.

Missing Claim Submission Deadlines

Even if you have eligible expenses, failing to submit your reimbursement claims by the specified deadline will result in forfeiture of those funds. This deadline is typically a few months after the plan year ends.

Many Flexible Spending Accounts participants incur expenses but delay submitting claims, sometimes forgetting altogether. This can lead to frustration and financial loss despite having correctly allocated funds.

Set reminders throughout the year and, especially, at year-end and during any grace period to submit all pending claims promptly. The sooner you submit, the sooner you get reimbursed.

The Future of Flexible Spending Accounts: What to Expect Beyond 2026

While we focus on 2026, it’s beneficial to consider the broader landscape of Flexible Spending Accounts and potential future developments. Regulatory changes and economic shifts can influence these benefit programs.

Historically, contribution limits tend to increase incrementally with inflation, ensuring the accounts remain relevant for rising healthcare costs. However, major legislative changes could introduce new features or restrictions.

Staying informed about proposed legislation or IRS guidance will be crucial for long-term financial planning involving FSAs and other tax-advantaged accounts.

Potential Regulatory Changes

The regulatory environment for Flexible Spending Accounts has seen various adjustments over the years, from the inclusion of over-the-counter medications to the introduction of carryover options. Future changes could impact eligibility or eligible expenses.

Advocacy groups often push for expansions of eligible expenses, such as certain wellness programs or specific medical devices. Conversely, budget considerations could lead to tighter restrictions.

Monitoring official IRS announcements and legislative updates from Congress will provide the most accurate insight into any upcoming modifications to Flexible Spending Accounts rules.

Impact of Healthcare Trends

Broader trends in healthcare, such as the increasing popularity of telehealth or advancements in medical technology, could influence what is considered an eligible FSA expense. As healthcare evolves, so too might the definitions of covered services.

The emphasis on preventive care and mental health services might also lead to expansions in eligible expenses. This could make FSAs even more versatile for comprehensive health management.

Employers may also adapt their Flexible Spending Accounts offerings in response to employee demand and competitive benefits landscapes, potentially introducing new features or enhancing existing ones.

| Key Aspect | Brief Description |

|---|---|

| Tax Savings | Contributions are pre-tax, reducing taxable income for significant savings. |

| Use-It-or-Lose-It | Unused funds are typically forfeited, unless grace period or carryover applies. |

| Eligibility | Employer-sponsored benefit for qualified medical or dependent care expenses. |

| 2026 Limits | Anticipate slight increases; verify official IRS announcements for exact figures. |

Frequently Asked Questions About 2026 Flexible Spending Accounts

The primary benefits of an FSA in 2026 include significant tax savings, as contributions are made pre-tax, lowering your taxable income. It allows you to pay for eligible healthcare and dependent care expenses with money that has not been taxed, maximizing your purchasing power for these essential services.

To determine your 2026 FSA contribution, carefully estimate your anticipated eligible healthcare and dependent care expenses for the year. Review past spending, consider any upcoming medical procedures, and factor in changes to your family’s needs. Be realistic, and consult your plan administrator for detailed eligible expense lists.

If you don’t use all your FSA funds by the end of 2026, you generally risk forfeiting the remaining balance due to the ‘use-it-or-lose-it’ rule. However, many employers offer either a grace period (extending the spending time) or a carryover option (allowing a limited amount to roll into the next year). Check your plan’s specifics.

Yes, over-the-counter medications are generally eligible for FSA reimbursement in 2026 without a prescription, a change that was made permanent. This includes items like pain relievers, cold medicines, and allergy treatments. Always keep your receipts and confirm eligibility with your specific FSA plan administrator for clarity.

Yes, if both spouses are employed and their respective employers offer FSAs, each spouse can contribute up to the maximum individual limit for a medical FSA in 2026. For Dependent Care FSAs, the limit is typically per household, meaning the combined contributions cannot exceed the household maximum, usually $5,000.

What this means

The landscape for Flexible Spending Accounts emphasizes proactive planning and informed decision-making.

Staying abreast of contribution limits, eligible expenses, and employer-specific rules is critical for leveraging these tax-advantaged benefits effectively.

Future adjustments in regulations or healthcare trends could further refine FSA utility, making continuous monitoring of official announcements essential for all participants and their financial well-being.

& IRA Limits")